TSMC: 7nm Now Biggest Share of Revenue

by Ian Cutress on January 17, 2019 9:00 AM EST- Posted in

- Semiconductors

- TSMC

- 7nm

- CLN7FF

- Revenue

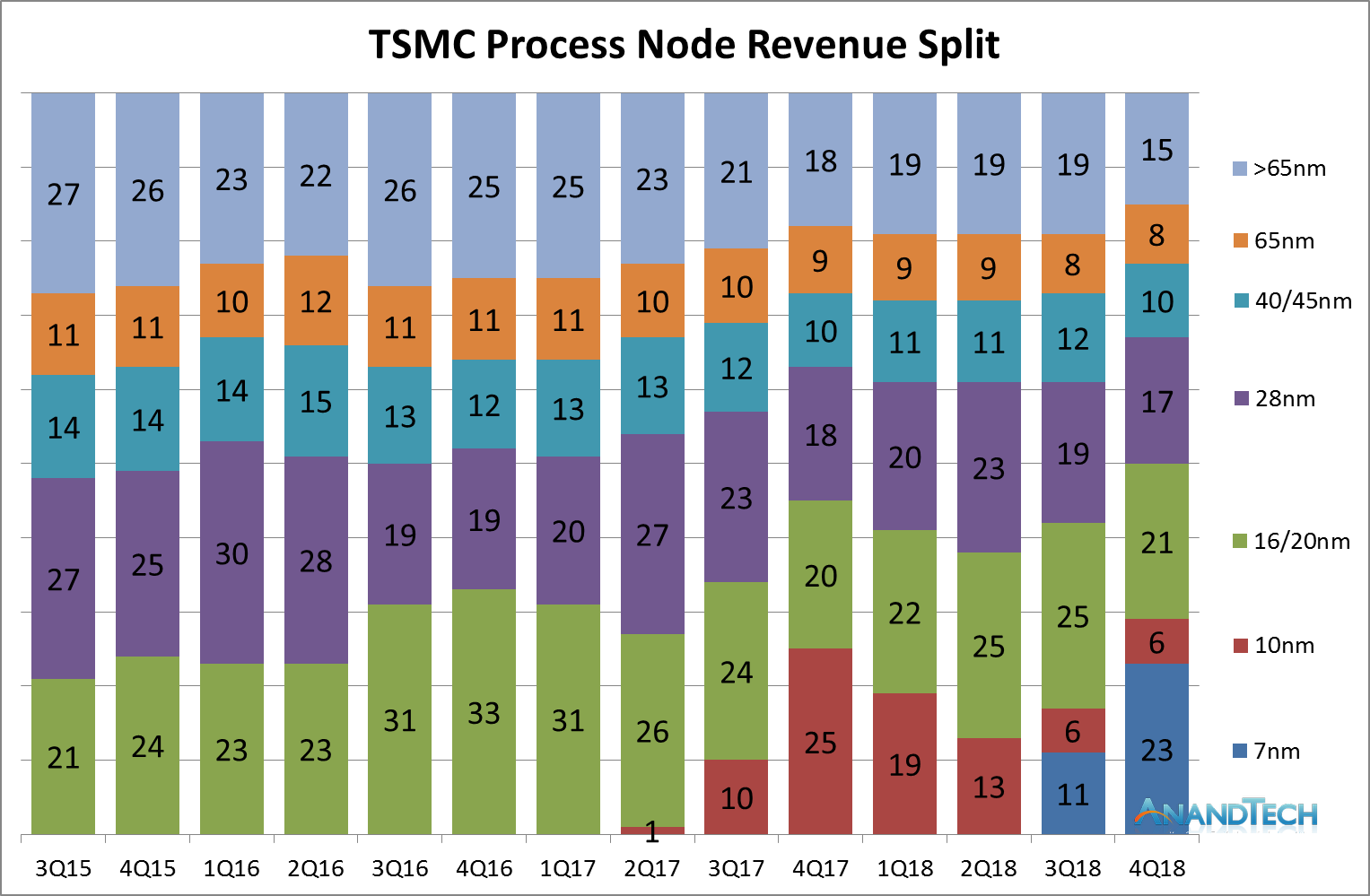

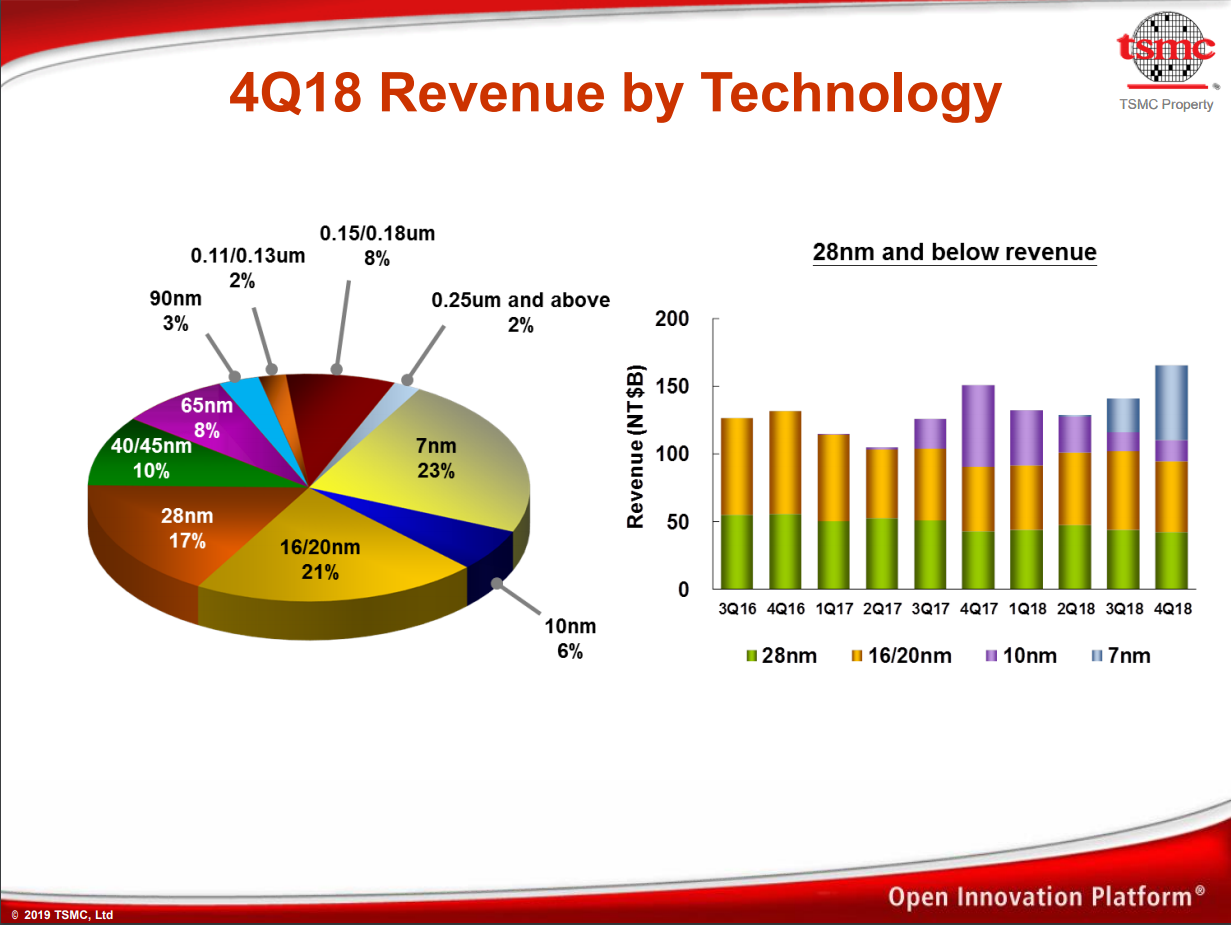

As process node technology gets ever more complex, it costs big dollars to develop and then building chips on the process is also a very costly process. The big foundries often have many process nodes running in parallel across a wide range of price brackets in order to both diversify the revenue streams but also offer multiple competitive options for the market. The latest numbers out of TSMC are stating that in Q4, the revenue generated from their leading edge 7nm node family now takes the biggest percentage of revenue for the company.

As posted by David Schor of WikiChip over Twitter, taking data from TSMC’s earning calls over the years and adding its latest Q4 results to the mix, it shows that 7nm has had a significant ramp, becoming 23% of the revenue of the company since it starting offering it as a process. Over the course of 2018, TSMC has stated that 7nm has accounted for close to 10% of total revenue, and the company expects the process node to be worth ‘greater than 20%’ of its 2019 revenue.

In the Q3 earnings call, CC Wei from TSMC stated that:

This is the first time in the semiconductor industry the most advanced logic technology is available for all product innovations at the same time. We continue to work with many customers on N7, N7+ product design and expect to see more than 100 customer product tape-outs by end of 2019 expect 7-nanometer to be a multiple waves of customer adoptions.

Trendforce has reported that TSMC held 56.1% of the worldwide market share for semiconductor foundry business in the first half of 2018, prior to 7nm being offered. Compared to other foundries, the same report has that GlobalFoundries holds 9.0% of the market, UMC at 8.9%, Samsung at 7.4%, and SMIC at 5.9%; all other players are sub 2.5%. It will be interesting to see if 7nm changes this balance.

On the future of 7nm offerings, back in August 2018, GlobalFoundries announced that it has stopped all 7nm development, that it no longer has plans to develop a 7nm process, and will focus on its current profit-generating technologies such as 14LPP, 12LP, 22FDX, and 12FDX. Also, Samsung’s 7nm offerings are starting to come online and the company has been particularly aggressive about discussing future process node technologies. We have also reported on TSMC's future plans, such as offering 5nm volume production by early 2020.

44 Comments

View All Comments

name99 - Thursday, January 17, 2019 - link

Huawei Kirin 970 is TSMC 10nm.Mediatek Helio X30

Qualcom Centriq and Snapdragon 700 are on Samsung 10nm

https://en.wikichip.org/wiki/10_nm_lithography_pro...

Dvgeniy - Thursday, January 17, 2019 - link

HiSillicin aka Huawei used TSMC 10nm.ilt24 - Thursday, January 17, 2019 - link

It seems their numbers are now heavily dependent on iPhone sales. In Q4 2017 Apple sold 77M iPhones, followed by 52M in Q1'18 and 41M in Q2'18cpkennit83 - Thursday, January 17, 2019 - link

Samsung's 10nm had more volume i think. It got both the 835 and 845, while tsmc got apple and kirin.eva02langley - Thursday, January 17, 2019 - link

They have more than 50% of the world business. At this point, Samsung is like an AMD vs Intel.Dvgeniy - Thursday, January 17, 2019 - link

Apple is more volume than 835 and 845 combinedname99 - Thursday, January 17, 2019 - link

The ignorance of some really is something, isn't it?You have UTTERLY NO clue how TSMC does business, do you?

Some questions

(a) do you think that TSMC lost money on 10nm? Even now, before considering that it will continue to be used for some purpose for years to come?

(b) do you think that TSMC could deliver such reliable execution, year after year (compared to, eg, Intel) if they didn't take these intermediate steps?

(c) do you think Apple and Huawei were unhappy with the chips they delivered on 10nm?

You're like some Dilbert middle manager who arrives at a building site and says that "obviously scaffolding is a waste of money, because it's gone by the time the building is finished! Next time we'll save so much money and time by not bothering to install it at all"...

Dvgeniy - Thursday, January 17, 2019 - link

Totally agree on (b) and (c). However (a) is arguable. Their gross margin on 10nm probably never reached corporate average, since it takes a year or so. And not likely to see new tape-outs on 10nm when you have much better 7nm available.drexnx - Friday, January 18, 2019 - link

actually I do have a clue - they amortize their extreme capital expenses across when something is an expensive leading node, then make boatloads of cash on the fully depreciated process lines 2+ jumps behind leading edge.know what that strategy depends on? keeping the line running as long as possible, leading edge or not.

Do YOU think TSMC was happy with their 10nm process being functionally dead a year after introduction? nothing else will tape out on 10nm, and why would anyone use it now?

They'll either go 16nm for cost, or 7nm and live with SADP if they really need it. no arguing whether it was necessary or not (obviously it was) but that it was necessary and that they used it doesn't mean it wasn't also a disappointment overall.

Dvgeniy - Friday, January 18, 2019 - link

Agree. The node was basically made for Apple. Hisilicon is a bonus. So they probably expected much longer volume commitments from the customer. On the bright side, they could reuse all the equipment for 7nm. So at the end of the day they are even.