AMD Reports Q2 2021 Earnings: Company-wide Growth Drives Doubled Revenue

by Ryan Smith on July 27, 2021 5:25 PM EST- Posted in

- CPUs

- AMD

- GPUs

- Financial Results

- Xilinx

Continuing our Q2 earnings coverage this month, AMD is next out the gate in reporting their earnings. And, has been the story now for most of the last year, AMD is enjoying explosive revenue growth across the company. CPU, GPU, and semi-custom sales are all up, pushing the limits of what AMD can do amidst the current chip crunch, and pushing the company to new levels of profitability in the process.

For the second quarter of 2021, AMD reported $3.85B in revenue, making for yet another massive jump over a year-ago quarter for AMD, when the company made just $1.93B in a then-record quarter. Now, half-way through 2021, AMD’s financial trajectory is all about setting (and beating) records for the company, as evidenced by the 99% leap in year-over-year revenue – falling just millions short of outright doubling their revenue.

AMD’s big run-up in revenue is also reflected in the company’s other metrics; along with that revenue AMD’s net income has grown by 352% year-over-year, now reaching $710M. And if not for an unusual, one-off tax benefit for AMD’s Q4’2020, this would have been AMD’s most profitable quarter ever – and indeed is on a non-GAAP basis. Meanwhile, as you might expect from such high net income figures, AMD’s gross margin has risen even further and now sits at 48%, up 4 percentage points from the year-ago quarter and 2 points from last quarter.

| AMD Q2 2021 Financial Results (GAAP) | |||||||

| Q2'2021 | Q2'2020 | Q1'2021 | Y/Y | Q/Q | |||

| Revenue | $3.85B | $1.93B | $3.45B | +99% | +12% | ||

| Gross Margin | 48% | 44% | 46% | +4pp | +2pp | ||

| Operating Income | $831M | $173M | $662M | +380% | +26% | ||

| Net Income | $710M | $157M | $555M | +352% | +28% | ||

| Earnings Per Share | $0.58 | $0.13 | $0.45 | +346% | +29% | ||

Breaking down AMD’s results by segment, we start with Computing and Graphics, which encompasses their desktop and notebook CPU sales, as well as their GPU sales. That division booked $2.25B in revenue for the quarter, $883M (65%) more than Q2 2020. Accordingly, the segment’s operating income is (once more) up significantly as well, going from $200M a year ago to $526M this year.

As always, AMD doesn’t provide a detailed breakout of information from this segment, but they have provided some selective information on revenue and average selling prices (ASPs). Overall, client CPU sales have remained strong; client CPU ASPs are up on both a quarterly and yearly basis, indicating that AMD has been selling a larger share of high-end (high-margin) parts. According to AMD this is the case for both desktop and laptop sales, and making this the fifth straight quarter of revenue share gains.

Meanwhile the company is reporting similarly good news from their GPU business. As with CPUs, ASPs for AMD’s GPU business as up on both a yearly and quarterly basis. According to the company this is being driven by demand for high-end Radeon 6000 video cards, as well as AMD Instinct (data center) sales. AMD began initial shipments of their first CDNA 2 architecture-based Instinct accelerators in Q2, opening the spigot there for data center GPU revenue going into Q3.

| AMD Q2 2021 Reporting Segments | |||||

| Q2'2021 | Q2'2020 | Q1'2021 | |||

|

Computing and Graphics

|

|||||

| Revenue | $2250M | $1367M | $2100M | ||

| Operating Income | $526M | $200M | $485M | ||

|

Enterprise, Embedded and Semi-Custom

|

|||||

| Revenue | $1600M | $565M | $1345M | ||

| Operating Income | $398M | $33M | $277M | ||

Moving on, AMD’s Enterprise, Embedded, and Semi-Custom segment has once again experienced a quarter of rapid growth, thanks to the success of AMD’s EPYC processors and demand for the 9th generation consoles. This segment of the company booked $1.6B in revenue, $1035M (183%) more than what they pulled in for Q2’20, and 19% ahead of an already impressive Q1’21. The big jump in revenue also means that the segment is even further into the black on an operating income basis, continuing to close the gap with the Computing and Graphics segment even with the all-around growth.

Overall, both the enterprise and semi-custom sides of this segment are up on a yearly basis. AMD set another record for server processor revenue this quarter on the strength of EPYC processor sales. Meanwhile semi-custom revenue was up on both a yearly and a quarterly basis, reflecting the continued demand for the latest generation of consoles.

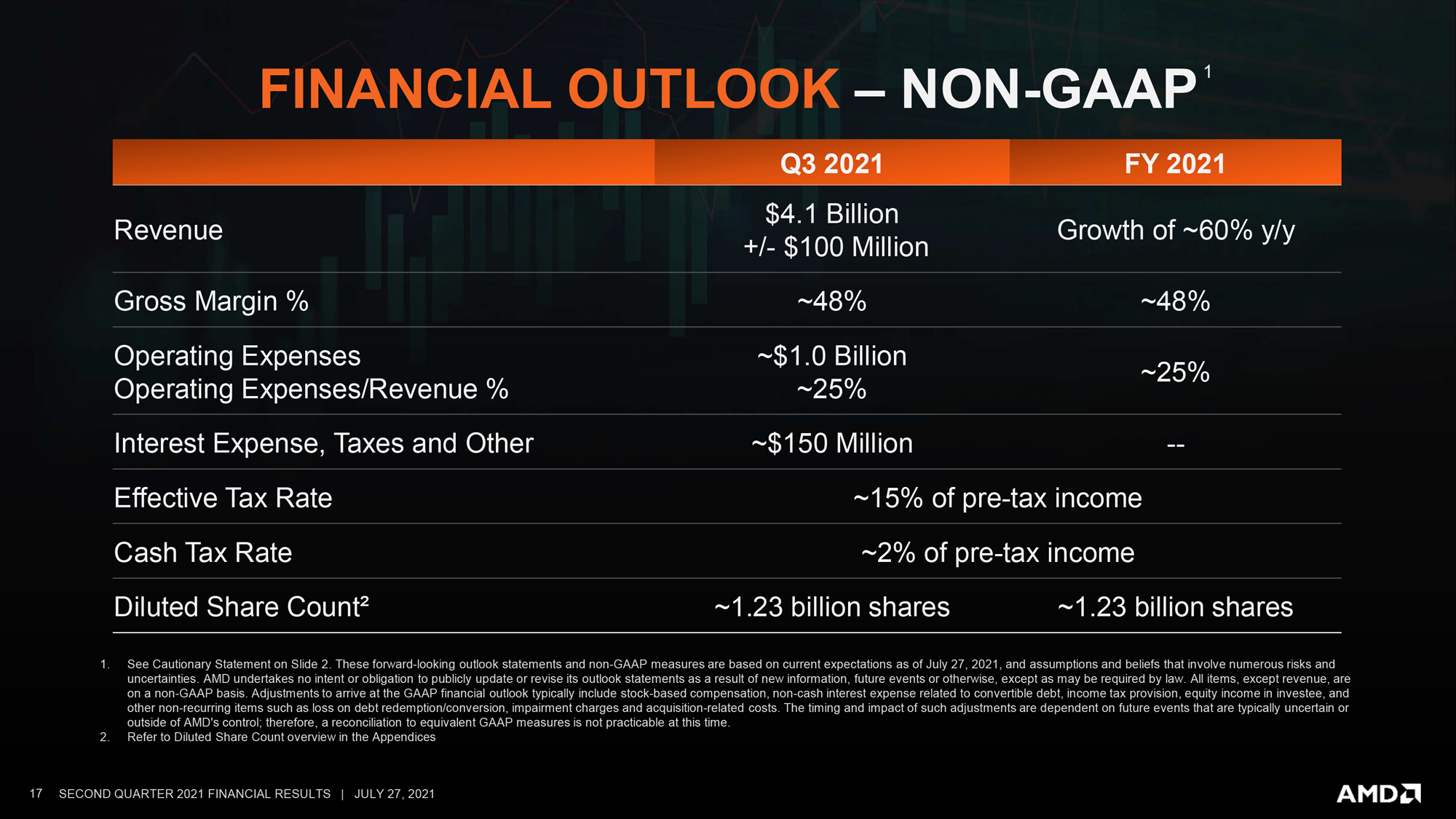

Looking forward, AMD’s expectations for the quarter and for the rest of the year have been bumped up once again. For Q3 the company expects to book $4.1B (+/- $100M) in revenue, which if it comes to pass will be 46% growth over Q3’20. Meanwhile AMD’s full year 2021 projection now stands at a 60% year-over-year increase in revenue versus their $9.8B FY2020, which is 10 percentage points higher than their forecast from the end of Q1.

Finally, while AMD doesn’t have any major updates on the ongoing Xilinx acquisition, the company has reiterated that it remains on-track. Which means that if all goes according to plan, it will close by the end of the year.

Source: AMD

104 Comments

View All Comments

eva02langley - Wednesday, July 28, 2021 - link

Their problem is their fabs and they are now making it a business. Their main competitor is not AMD, it is TSMC. If you think TSMC is just going to sit still and let Intel do their things, then you don't get it. Intel will never get the node advantage back, they are 3-4 years behind TSMC.They need TSMC to drop the ball for 3-4 years to catch them up, this is how bad it is. Putting an Engineer as CEO will not change this. Hope is not a strategy!

mode_13h - Wednesday, July 28, 2021 - link

> Still don't understand how Intel lost such a big lead, what were their engineers upto?It's been said many times: Intel has been extracting value from the company for many years. They spend a lot of their profits on dividends and share buy-backs, then turn around and do rounds of layoffs to keep costs down. The result can hardly be surprising.

TheinsanegamerN - Wednesday, July 28, 2021 - link

That's nto all they did though. Intel has also invested billions into the 10nm process trying to get it to work properly, and is still investing billiosn into further R+D and fab capacity.AMD got really lucky that intel ran into so many roadblocks with 10nm production.

Teckk - Thursday, July 29, 2021 - link

Doesn’t take away the good designs of Zen and chiplet architecture that Intel mocked to actually do the same thing going forward.TheinsanegamerN - Thursday, July 29, 2021 - link

Nice red herring. I never said it did, and what AMD has done with zen has no bearing on wht intel wa sspending money on this whole time.mode_13h - Sunday, August 1, 2021 - link

> what AMD has done with zen has no bearing on wht intel wa sspending money on this whole time.I'm not so sure about that. If Zen wasn't so strong, I think it wouldn't have created quite the same urgency, on Intel's part. Zen could turn out to be the best thing to happen to Intel, if the whole management shakeup and reallocation of funding wouldn't have happened (or at least to the same degree), otherwise.

Makste - Saturday, July 31, 2021 - link

It is not pure luck though. There's execution. Supposing intel had it's 10nm up and running in 2016, Zen and the chiplet architecture was still going to come out, it could have taken longer for adoption maybe, but all the advantages and disadvantages between the two were going to be compared against each other still, and AMD would still be a tough competitor with that zen uarchAzix - Tuesday, July 27, 2021 - link

Is the word frontloading? Their revenue will drop later as demand drops and competition heats up.eva02langley - Wednesday, July 28, 2021 - link

Next quarter will stay flat... - AMD.No drop here...

Teckk - Thursday, July 29, 2021 - link

Competition goes both ways :)