AMD Reports Q2 2021 Earnings: Company-wide Growth Drives Doubled Revenue

by Ryan Smith on July 27, 2021 5:25 PM EST- Posted in

- CPUs

- AMD

- GPUs

- Financial Results

- Xilinx

Continuing our Q2 earnings coverage this month, AMD is next out the gate in reporting their earnings. And, has been the story now for most of the last year, AMD is enjoying explosive revenue growth across the company. CPU, GPU, and semi-custom sales are all up, pushing the limits of what AMD can do amidst the current chip crunch, and pushing the company to new levels of profitability in the process.

For the second quarter of 2021, AMD reported $3.85B in revenue, making for yet another massive jump over a year-ago quarter for AMD, when the company made just $1.93B in a then-record quarter. Now, half-way through 2021, AMD’s financial trajectory is all about setting (and beating) records for the company, as evidenced by the 99% leap in year-over-year revenue – falling just millions short of outright doubling their revenue.

AMD’s big run-up in revenue is also reflected in the company’s other metrics; along with that revenue AMD’s net income has grown by 352% year-over-year, now reaching $710M. And if not for an unusual, one-off tax benefit for AMD’s Q4’2020, this would have been AMD’s most profitable quarter ever – and indeed is on a non-GAAP basis. Meanwhile, as you might expect from such high net income figures, AMD’s gross margin has risen even further and now sits at 48%, up 4 percentage points from the year-ago quarter and 2 points from last quarter.

| AMD Q2 2021 Financial Results (GAAP) | |||||||

| Q2'2021 | Q2'2020 | Q1'2021 | Y/Y | Q/Q | |||

| Revenue | $3.85B | $1.93B | $3.45B | +99% | +12% | ||

| Gross Margin | 48% | 44% | 46% | +4pp | +2pp | ||

| Operating Income | $831M | $173M | $662M | +380% | +26% | ||

| Net Income | $710M | $157M | $555M | +352% | +28% | ||

| Earnings Per Share | $0.58 | $0.13 | $0.45 | +346% | +29% | ||

Breaking down AMD’s results by segment, we start with Computing and Graphics, which encompasses their desktop and notebook CPU sales, as well as their GPU sales. That division booked $2.25B in revenue for the quarter, $883M (65%) more than Q2 2020. Accordingly, the segment’s operating income is (once more) up significantly as well, going from $200M a year ago to $526M this year.

As always, AMD doesn’t provide a detailed breakout of information from this segment, but they have provided some selective information on revenue and average selling prices (ASPs). Overall, client CPU sales have remained strong; client CPU ASPs are up on both a quarterly and yearly basis, indicating that AMD has been selling a larger share of high-end (high-margin) parts. According to AMD this is the case for both desktop and laptop sales, and making this the fifth straight quarter of revenue share gains.

Meanwhile the company is reporting similarly good news from their GPU business. As with CPUs, ASPs for AMD’s GPU business as up on both a yearly and quarterly basis. According to the company this is being driven by demand for high-end Radeon 6000 video cards, as well as AMD Instinct (data center) sales. AMD began initial shipments of their first CDNA 2 architecture-based Instinct accelerators in Q2, opening the spigot there for data center GPU revenue going into Q3.

| AMD Q2 2021 Reporting Segments | |||||

| Q2'2021 | Q2'2020 | Q1'2021 | |||

|

Computing and Graphics

|

|||||

| Revenue | $2250M | $1367M | $2100M | ||

| Operating Income | $526M | $200M | $485M | ||

|

Enterprise, Embedded and Semi-Custom

|

|||||

| Revenue | $1600M | $565M | $1345M | ||

| Operating Income | $398M | $33M | $277M | ||

Moving on, AMD’s Enterprise, Embedded, and Semi-Custom segment has once again experienced a quarter of rapid growth, thanks to the success of AMD’s EPYC processors and demand for the 9th generation consoles. This segment of the company booked $1.6B in revenue, $1035M (183%) more than what they pulled in for Q2’20, and 19% ahead of an already impressive Q1’21. The big jump in revenue also means that the segment is even further into the black on an operating income basis, continuing to close the gap with the Computing and Graphics segment even with the all-around growth.

Overall, both the enterprise and semi-custom sides of this segment are up on a yearly basis. AMD set another record for server processor revenue this quarter on the strength of EPYC processor sales. Meanwhile semi-custom revenue was up on both a yearly and a quarterly basis, reflecting the continued demand for the latest generation of consoles.

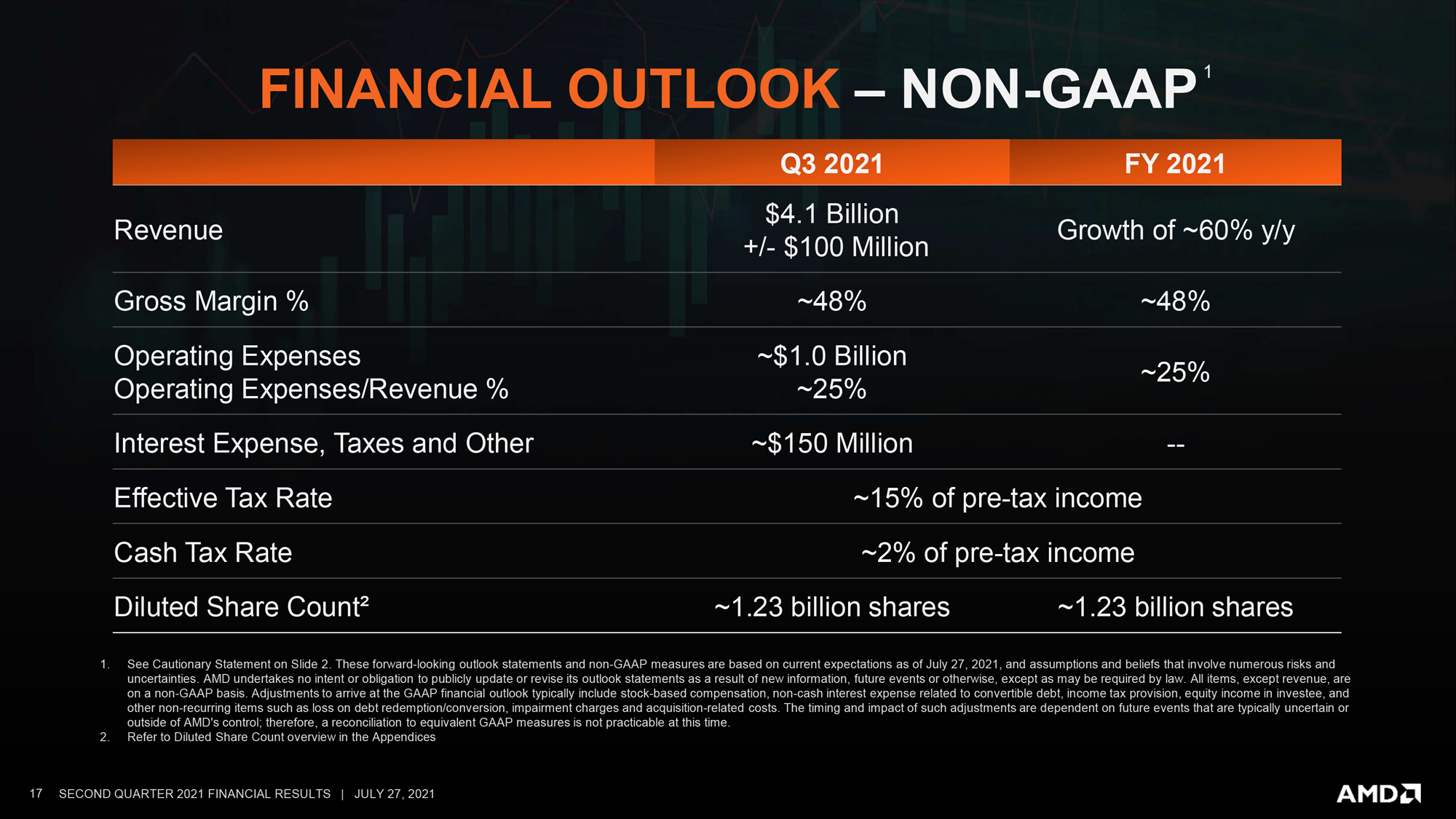

Looking forward, AMD’s expectations for the quarter and for the rest of the year have been bumped up once again. For Q3 the company expects to book $4.1B (+/- $100M) in revenue, which if it comes to pass will be 46% growth over Q3’20. Meanwhile AMD’s full year 2021 projection now stands at a 60% year-over-year increase in revenue versus their $9.8B FY2020, which is 10 percentage points higher than their forecast from the end of Q1.

Finally, while AMD doesn’t have any major updates on the ongoing Xilinx acquisition, the company has reiterated that it remains on-track. Which means that if all goes according to plan, it will close by the end of the year.

Source: AMD

104 Comments

View All Comments

mode_13h - Wednesday, July 28, 2021 - link

> AMD began initial shipments of their first CDNA 2 architecture-based> Instinct accelerators in Q2,

Of course, you wouldn't know this if you relied solely on Anandtech for tech news.

: (

> opening the spigot there for data center GPU revenue going into Q3.

Well, not exactly. They have a "software pipeline" problem that basically none of their consumer hardware is supported by their compute stack, so basically the only ones porting anything to it are AMD employees and probably a few grad students working as interns on the couple HPC wins AMD landed.

The genius move Nvidia made was to fully support CUDA on their entire hardware range, from top to (almost) bottom. Sometimes, their very lowest-end card doesn't support it, but even their Jetson embedded compute modules can run it.

Intel is doing one better than Nvidia, by supporting their compute APIs on CPUs, GPUs, FPGAs, and (where appropriate) hardware AI chips.

As long as AMD considers cloud and HPC as their only compute customers, adoption even in those segments is going to be limited. And as adoption of purpose-built AI hardware starts to gain momentum, AMD is going to see sales of their CDNA products hit a brick wall.

Ryan Smith - Wednesday, July 28, 2021 - link

"Of course, you wouldn't know this if you relied solely on Anandtech for tech news."There isn't anything to report on that front. AMD isn't saying a thing about CDNA 2 other than that they've shipped some parts to someone, somewhere.

mdriftmeyer - Wednesday, July 28, 2021 - link

Why would they reveal specific customer sales of the MI200? Have they done that with Radeon? No. The fact the product is ready and targeted for major compute markets, especially Supercomputer clients that have already been published should be a clue who is using them.Ryan Smith - Wednesday, July 28, 2021 - link

Oh, we're aware of where they're (likely) going. The point is more to underscore how little AMD is saying about CDNA 2 parts right now.mode_13h - Wednesday, July 28, 2021 - link

> There isn't anything to report on that front. AMD isn't saying a thing about CDNA 2Thanks for confirming. Not to sound ungrateful, but um, what about CDNA 1 (MI100) coverage? As I recall, there've also been a few other GPUs that launched without coverage on this site.

eva02langley - Wednesday, July 28, 2021 - link

The "GENIUS" Nvidia move is now biting them in the ass, because ampere is hosting double the cores and offer 40% performance uplift. They are facing a GCN moment where they don't have a gaming uarch anymore... and they lost the entire gaming market. Holding the dGPU business is nothing if studios don't use your hardware beside when you bribe them to implement your tech.Don't lure yourself, games are made on consoles now. FSR adoption will skyrocket with the console adoption to. Nvidia cornered themselves with DLSS and RTX to paint AMD as the duck, but now with FSR, it literally backfired royally.

Spunjji - Wednesday, July 28, 2021 - link

For a company that's "lost" the gaming market, Nvidia sure do seem to be doing just fine selling every gaming card they makemode_13h - Wednesday, July 28, 2021 - link

You can tell they're hurting by the aggressive price breaks. I mean, they can hardly be making any money on those GPUs!; )

mode_13h - Wednesday, July 28, 2021 - link

They do nerf some their consumer cards in some ways that are important for professional users.But, the key point is that you can still use consumer cards for development & dabbling with the whole Nvidia software stack. This is important for getting kids in university to port & optimize open source software for your hardware.

Much of the goodwill AMD built by having an open source driver stack, they've lost by stumbling so badly with lacking compute support for consumer hardware. Just checkout any discussion of ROCm on pretty much any site, and you'll find much gnashing of teeth about this.

Oxford Guy - Wednesday, July 28, 2021 - link

Goodwill for those who invested when the company was cheap. Goodwill for those who care about efficient CPUs and not high-performance gaming.Anti-goodwill for the few consumers who have a clue about things like:

— designing GPUs to sell to mining first and foremost

— selling junk at the ‘high end’ so Nvidia can raise prices, the junk that didn’t go to miners will be purchased by foolish ‘team red’s, and the high prices of PC gaming will sell more PCs in disguise — that AMD happens to allocate so many wafers to.

— sandbagging for many years at the midrange and above areas, to, additionally, raise prices with Nvidia via pent-up demand, not be so obvious in the various anti-PC enthusiast schemes (once actually competitive cards are deigned to be produced — just by chance during the great shortage), and be hailed as amazing for the technical wizardry of actually bothering to release something competitive for the first time since Hawaii.

— Goodwill for those invested in MS and Sony.